WHAT WE LEARNED IN MAY: TRADE POLICY CONTINUES TO CLOUD OUTLOOK

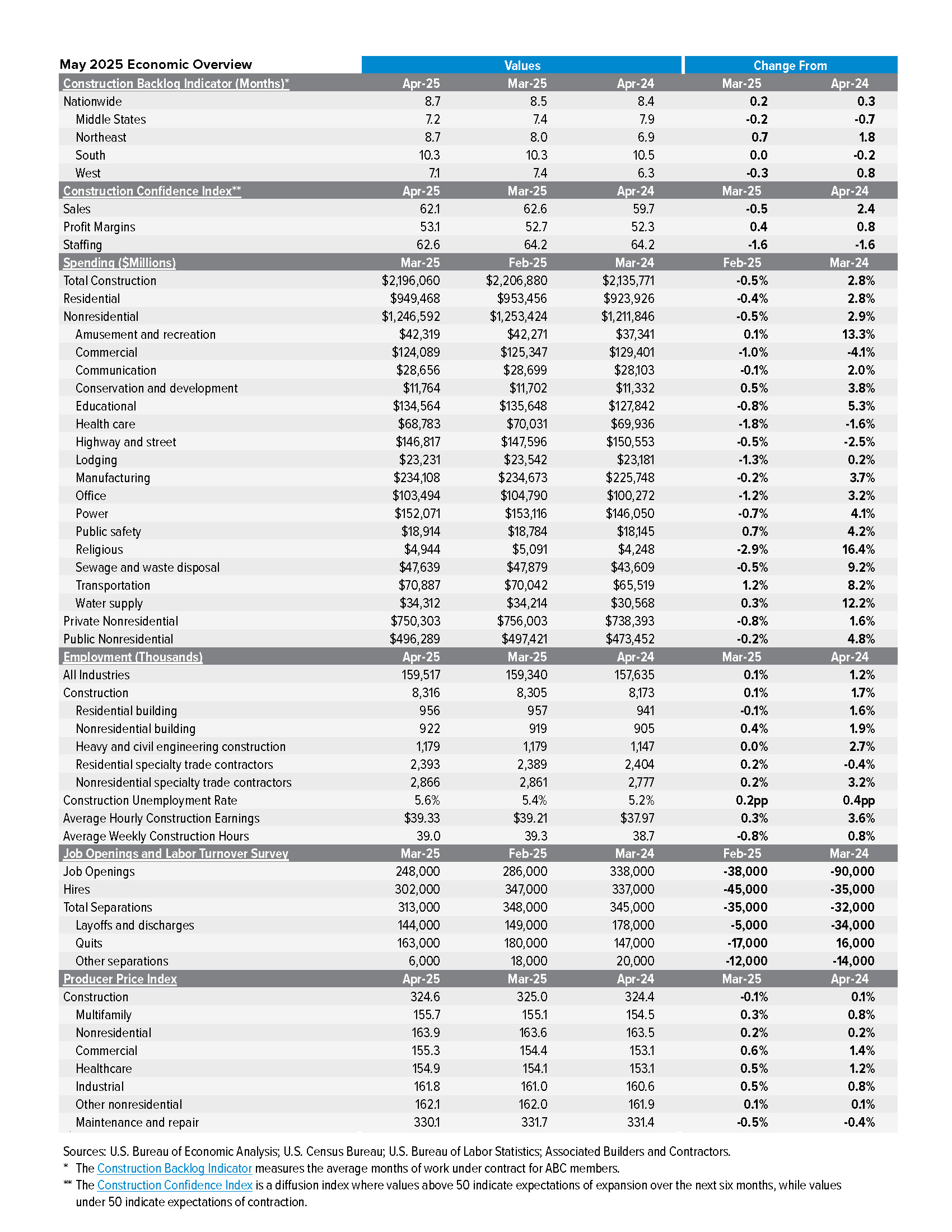

Construction-specific economic data released in May provide mixed signals. Nonresidential construction spending fell sharply in April, and industrywide job openings are down significantly over the past year. At the same time, backlog rose to a 20-month high, the industry continues to add jobs at a faster-than-economywide pace, and contractors are broadly optimistic about the next six months.

NONRESIDENTIAL CONSTRUCTION SPENDING PLUNGES IN MARCH

Nonresidential construction spending fell sharply in March, and the declines were spread across a majority of subsegments.Data center construction activity, which has accounted for about 70% of the increase in nonresidential spending over the past year, is one of the few sources of nonresidential momentum. While manufacturing related construction activity remains historically elevated, it has leveled off over the past year, rising just 3.7% since March 2024.

DESPITE RISING IRON AND STEEL PRICES, INPUT COSTS TAME FOR NOW

Overall construction input prices inched lower in April, but that’slargely due to falling oil prices. Inputs affected by recent changes in trade policy, like iron and steel, are experiencing rapid price escalation. While the 90-day pause on some tariffs on Chinese imports have reduced economic uncertainty, the 25% tax on steel and aluminum imports appears set to remain in place indefinitely. As a result, input prices will likely continue to rise in the coming months.

CONSTRUCTION EMPLOYMENT CONTINUES TO GROW DESPITE SIGNS OF WEAKENING DEMAND

Construction employment rose by another 11,000 positions in April, and the majority of that growth occurred in the nonresidential segment. Despite ongoing employment gains, the industry has 90,000 fewer job openings than it did one year ago, and the hiring rate fell to the lowest level ever recorded in March. These dynamics suggest that contractors are not reducing their staffing levels, but are hiring only when absolutely necessary.

BACKLOG RISES, CONTRACTORS REMAIN BROADLY OPTIMISTIC

ABC’s Construction Backlog Indicator increased to a 20-month high of 8.7 months in April, with almost all of the recent gains concentrated among contractors with greater than 0 million in annual revenues. Contractor confidence also remains elevated despite uncertainty related to trade policy. Notably, 22% of contractors had a project delayed or canceled in April due to tariffs, while 87% have been notified of tariff-related price increases.

LOOKING AHEAD

The recently announced 90-day reduction in tariffs on Chinese imports has improved the outlook and provided at least a sliver of clarity regarding the future path of trade policy. Even so, both uncertainty and import taxes remain significantly higher than at the end of 2024, and interest rates are expected to remain elevated in the near term despite softer inflation data in recent months. As a result, the nonresidential construction segment may struggle to gain momentum over the next several months.