What We Learned in March: Construction Industry Momentum Wavers

Nonresidential construction spending continues to inch higher while the industry keeps adding jobs at a healthy pace, but trade tensions, tariffs, rising material prices and higher-for-longer interest rates could weigh on the industry’s momentum throughout the remainder of 2025.

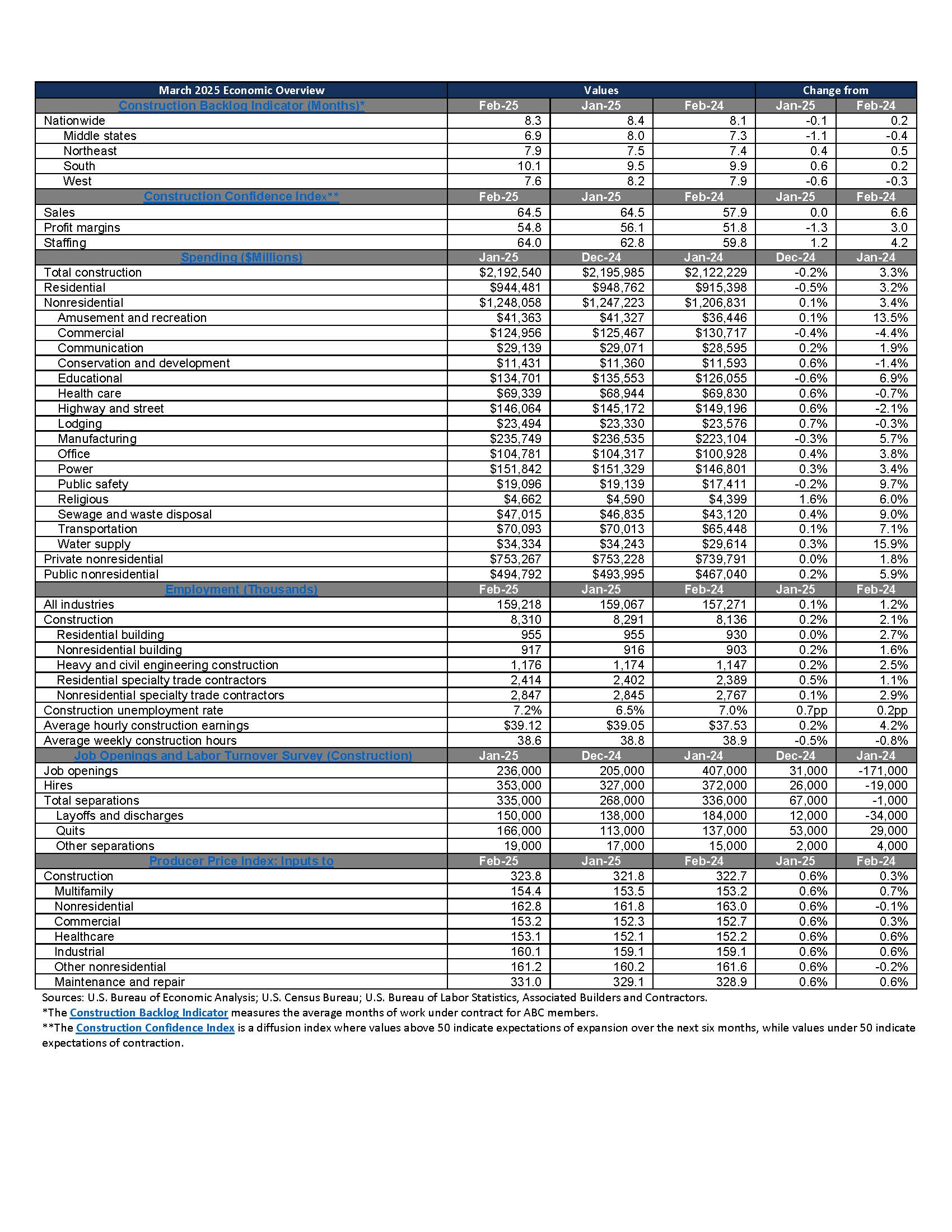

Input Costs Increase on Higher Iron and Steel Prices

Nonresidential construction input prices surged higher in February and have risen at a 9.0% annualized rate over the first two months of 2025. Tariffs are a primary factor behind the recent rise, as import taxes allow domestic producers to raise prices. Despite the increase over the past two months, nonresidential input prices are still down, albeit slightly, on a year-over-year basis.

Nonresidential Construction Spending Inches Higher in January

Nonresidential construction spending increased 0.1% in January, but more than three-fourths of that increase was due to the ongoing boom in data center construction. Momentum remains scarce across other nonresidential subsegments, and even manufacturing—which still accounts for about $1 in every $5 of nonresidential spending—is virtually unchanged since May of 2024.

Contractors Add 19,000 Jobs in February

Construction industry employment rose by 19,000 in February, with about two-thirds of that increase coming in the residential specialty trade contractor subsegment. While industrywide job openings remain relatively low, hiring, layoffs and quits all accelerated in early 2025, suggesting the recent period of subdued construction labor market churn is coming to an end.

Backlog Inches Lower, Contractors Remain Confident

ABC’s Construction Backlog Indicator inched down to 8.3 months in February, and that decline was due to weakening backlog with contractors earning less than $100 million in annual revenues. Despite the small decrease, contractors on net are optimistic that their sales, staffing levels and profit margins will expand over the next six months.

Looking Ahead

Economywide inflation decelerated slightly in February but remains too fast to support additional rate cuts. High borrowing costs, rising input prices and the potential effects of tariffs suggest that the cost of construction services will rise in the coming months.

Despite that potential headwind, contractors remain broadly optimistic. Spending and employment data have shown some minor indications of weakness, yet nothing to suggest an imminent contraction in construction activity.