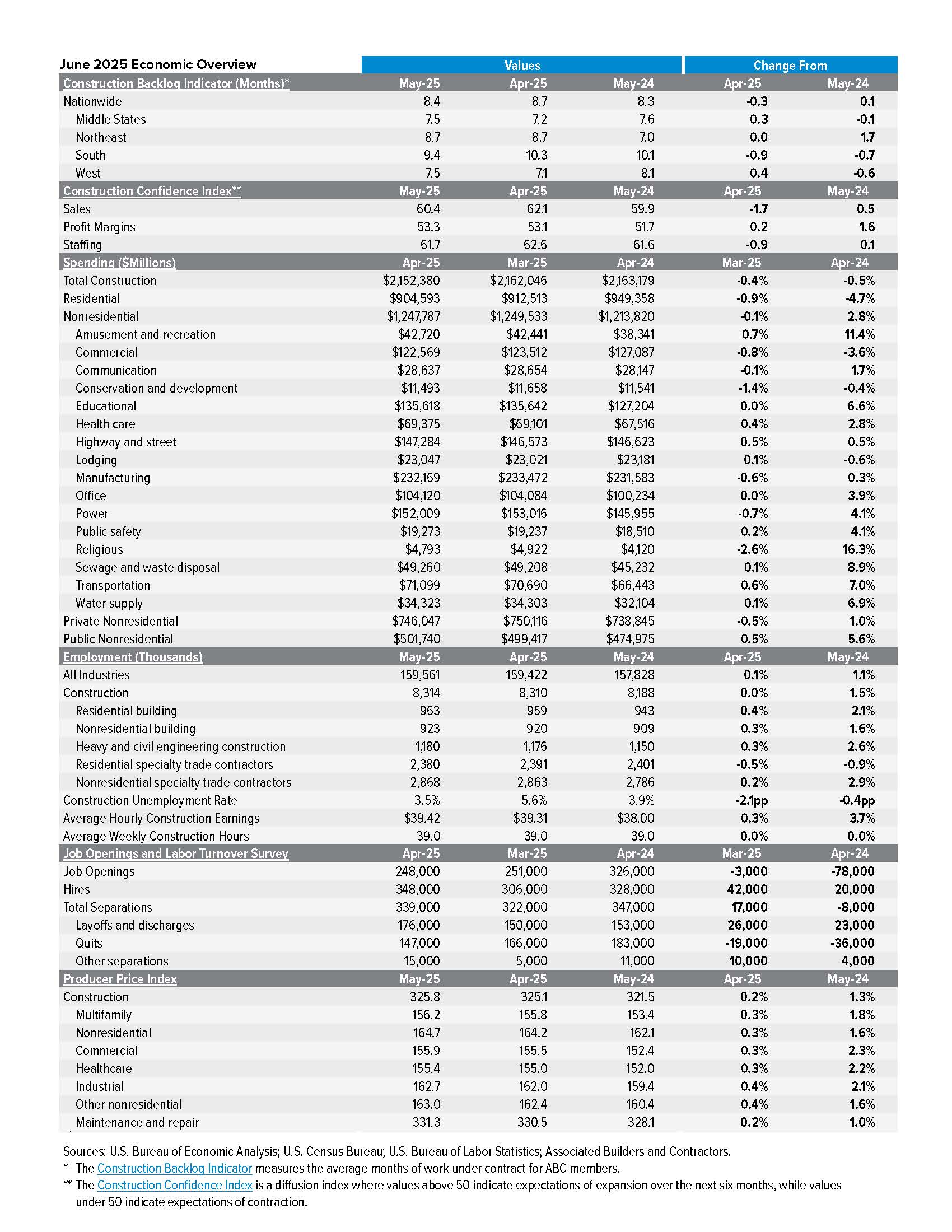

What We Learned in June: Some Signs of Waning Momentum

Construction-specific economic data have started to flash a few signs of potential weakness. Both backlog and nonresidential construction spending declined for the month, and while nonresidential employment continues to grow at a healthy pace, the residential segment is now contracting. While materials prices are still up just 1.3% over the past year, prices have risen too quickly over the first five months of 2025, especially those subject to elevated tariffs.

Nonresidential Construction Spending Slips in April

Nonresidential construction spending fell in April, with a particularly large decrease in private sector activity. Private nonresidential spending has now fallen in three of the first four months of 2025 and is on pace to decline 4% over the course of the year. While data center investment continues to rise, few other subsegments are currently exhibiting momentum.

Input Price Escalation Continues

Construction input prices continued to rise in May and have now increased at roughly a 6% annualized rate through the first five months of 2025. Emerging escalation is largely due to rapid price increases for tariff-affected goods like iron and steel, and this data predates the recent increase in iron and steel tariffs from 25% to 50%.

Nonresidential Contractors Continue to Hire

Nonresidential construction employment grew by 11,300 positions in May and has now increased at over twice the rate of the broader economy over the past year. The residential segment fared less well, losing more than 7,000 jobs in May as high interest rates weigh heavily on homebuilding activity.

Backlog Falls, Contractors Remain Confident

ABC’s Construction Backlog Indicator fell sharply from April’s 20-month high. Despite the decline, backlog remains 0.1 months above year-ago levels. Contractors remain broadly confident about the next six months, with sales, profit margin and staffing expectations all up on a year-over-year basis.

Looking Ahead

Despite emerging signs of weakness, contractors remain confident about the remainder of 2025. Softer-than-expected inflation data for May suggest that there could be more rate cuts than previously anticipated this year. If that occurs, lower borrowing costs will provide a welcome tailwind for the construction industry.

SEE ALSO: WHY CONSTRUCTION RELATIONSHIPS NEED A TRUST THERMOSTAT